Ontario Auto Reform 2026: What Optional Accident Benefits Change for Regulatory Reporting

By separating what was previously a largely standardized package of mandatory accident benefits, the Ontario auto insurance reform, effective Jul 1, 2026, gives drivers more choice over coverage and can affect premiums. Known as the new Statutory Accident Benefits Schedule (SABS), most accident benefits (AB) become optional coverages. For Ontario’s auto insurers, the new “à la carte” model presents an operational and reporting challenge: more benefit combinations, more edge cases, and more submission variance.

Key Reporting Changes Introduce New Complexity

Beyond a policy update, the reform, mandated by the Financial Services Regulatory Authority of Ontario (FSRA), is essentially a structural overhaul. While the total number of available benefits remains the same, the standard package shrinks significantly. With this comes various challenges for insurers, but from a compliance standpoint alone, it simply makes reporting more complicated. Insurers need a platform that can keep pace as new requirements unfold without resorting to manual workarounds or leading to inconsistent data downstream.

That’s where an evergreen regulatory reporting system matters: one that can be configured to reflect how a carrier writes business and one that can be updated as statistical plans change, so filings remain accurate, complete, and compliant.

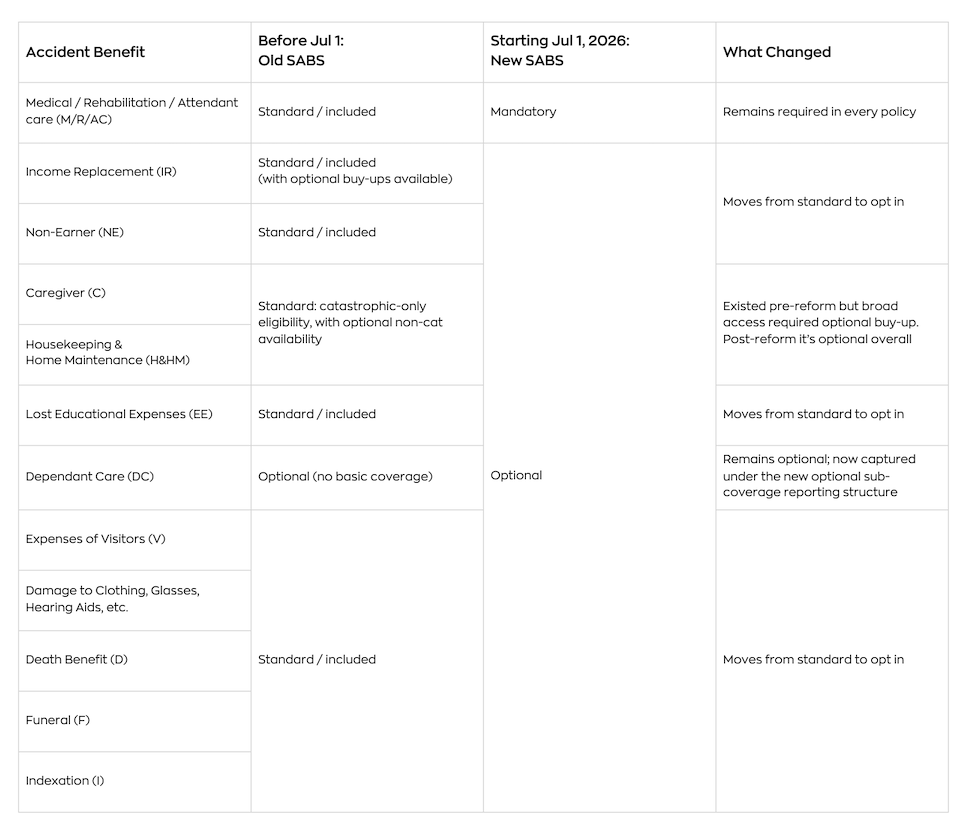

This table summarizes benefit availability for policyholders. Reporting implementation differs by plan: ASP introduces new accident benefit coverage/sub-coverage fields and retires legacy Ontario AB codes for policies effective July 1, 2026 and later; RSP uses updated grouping codes and blank-field rules within its existing submission format.

Detailed Impacts to Industry Reporting

Ontario’s auto reform doesn’t only modify coverage options; it also alters what insurers must capture, validate, and submit through statistical reporting. For many carriers, that work spans multiple source environments, including Guidewire Cloud, where coverage selections and billing structures may not translate directly into GISA’s revised Automobile Statistical Plan (ASP) or Facility Association’s (FA) Risk Sharing Pool (RSP) reporting. As the ASP updates to reflect Ontario’s AB reform, the operational burden concentrates in two parts of the workflow: standardizing source data into a consistent structure and applying updated reporting rules downstream as the statistical plan evolves.

Starting at the submission layer, GISA’s revised ASP submission layout expands from 600 bytes to approximately 1000 bytes (957, to be exact), reflecting additional fields insurers must capture and report under the new SABS structure. In practice, that means more data elements to populate, more valid combinations to account for, and more special cases to validate across both premium and claims records. Designed to absorb the expanded file layout and field positions, Hubio’s regul8’s business logic produces the required ASP output without structural rework. That’s the downstream side.

Upstream, the same reform creates new data-handling requirements inside the carrier’s own product and billing structures. The gap is that insurers may package optional accident benefits into product bundles to simplify the customer offering, while the ASP still requires reporting at the coverage level. Because the ASP now distinguishes the mandatory benefits by endorsement condition and because many optional benefits now include sub-coverages and option tiers, insurers must translate bundled product offerings into the discrete coverage and sub-coverage selections the ASP expects. RSP reporting follows the same direction: the file format stays intact, but the coding logic changes. regul8 handles that translation by decomposing product-level records into coverage-level records aligned to each carrier’s business rules so that the submission matches how GISA expects the data.

Most Common Reporting Scenarios under the Updated SABS

Here are a few specific instances that further illustrate what complexity looks like in real reporting workflows, and why an evergreen platform matters.

New Coverage and Sub-Coverage Reporting

The three accident benefits that remain mandatory are medical, rehabilitation, and attendant care (M/R/AC). While they’re individual benefit categories in claims handling, GISA’s revised ASP groups them into one bucket that puts M/R/AC under one of two codes, depending on whether an excluded driver endorsement applies. Pre-reform, M/R/AC were reported under a single code with one limit field for premium and one limit field for claims. Although the endorsement condition could apply contractually, they were not distinctly reflected in ASP reporting. Going forward, the new ASP reporting breaks this out by separating M/R/AC premium and claim records based on whether the endorsement applies, increasing the number of reporting variants insurers must produce and validate.

Similarly, caregiver (C) and housekeeping & home maintenance (H&HM), now both optional benefits, show how Ontario AB reporting is moving from indicator-style fields and legacy numeric codes to 7-alphanumeric coverage and sub-coverage reporting categories. Pre-reform, these benefits were largely represented through a simple numeric indicator approach (basic vs optional), even though eligibility differed depending on catastrophic versus non-catastrophic circumstances. Under the revised structure, that nuance becomes reportable through its own dedicated sub-coverage codes: C is captured using separate reporting categories (i.e., the eligibility of either catastrophic only or all impairment, the latter comprising catastrophic and non-catastrophic), and H&HM follows the same pattern. The result is more reporting variants, each requiring the correct premium and claim records to be produced, validated, and reconciled.

Another benefit worth noting is dependant care (DC), which brings a different reporting pattern than the “either/or” variants above (e.g., M/R/AC, C, H&HM). DC remains optional, but in the new structure it is reported under one sub-coverage code while still requiring multiple limit fields (first dependant and additional dependants). In other words, C and H&HM require insurers to select the correct reporting category based on coverage scope (catastrophic-only versus all injuries), whereas DC requires insurers to populate a single reporting category with the correct limit fields. This distinction matters because both patterns increase mapping and validation requirements — just in different ways — and both must align cleanly with downstream premium and claims reporting.

The reform also reinforces the first notice of loss (FNOL) rule, under which accident benefits are typically paid by the insurer responsible under Ontario’s priority of payment, often the insured’s own insurer, within the no-fault system. Through the revised OPCF 47R endorsement and rules governing priority of payment, eligible claimants may proceed under their own policy even where another party may be at fault, simplifying access to benefits from a consumer perspective. While this first-payer rule enhances protection and reduces friction when it comes to claiming, it increases operational burden as insurers must clearly identify responsible policies and reflect those accident benefits under the revised M/R/AC structure. This brings greater administrative and statistical rigour requirements within GISA submissions.

regul8 abstracts this structural variability by standardizing coverage, sub-coverage, and premium logic within its transformation layer, ensuring fully reconciled ASP submissions regardless of how carriers package or store benefits internally.

Updated Gender in Driver Classification

Unlike the endorsement-based split within the M/R/AC coverage, this driver-level change affects both rating inputs and statistical reporting. The reform introduces a Gender X designation within the Rated Operator Gender field, alongside the existing male and female classifications. At the same time, insurers that derive “Type of Use” codes must update the business rules that map rating attributes, including gender, to the corresponding reporting class. Type of Use represents actuarial rating classes determined by combinations of driver characteristics such as gender, age band, and operator status (principal or occasional), and serves as a key determinant of risk used in policy pricing. regul8 incorporates these logic updates so that drivers designated as Gender X are consistently classified and reported in accordance with the revised ASP reporting specifications.

Renewal Transaction Identification

Until now, renewals were reported using the same transaction code as new submissions, limiting lifecycle visibility in statistical data. As part of the reform, renewals receive their own transaction code, and cancellation of renewals is also assigned a different transaction code. This added granularity brings clarity to policy event reporting, allowing regulators to distinguish new from retained business, and supports better tracking of renewal behaviour, pricing dynamics, and overall market response to structural changes. Because regul8 centralizes transaction mapping within its transformation layer, carriers can implement these changes without restructuring their internal policy systems, ensuring seamless compliance with the updated ASP submission standards.

While narrower in scope than the changes to SABS coverage coding and field usage, updates to driver classification and renewal transaction identification strengthen reporting integrity. They ensure that rating variables and policy lifecycle events remain accurately reflected in statistical submissions as the reform takes effect.

The Effect on Risk Sharing Pool Reporting

RSP is Facility Association’s pooling mechanism for higher-risk private passenger vehicle (PPV) business of which premium-claim alignment depends on disciplined reporting. As Ontario’s auto reform requires more granular coverage elections and transaction distinctions, those changes extend into RSP reporting, where classification accuracy and timing discipline determine how ceded premiums and claims are ultimately aligned.

Reporting Segmentation & Classification Changes

One of the primary areas impacted by Ontario’s auto reform is the way business is segmented and classified for RSP reporting. However, to minimize disruption, Facility Association is keeping the RSP submission formats unchanged. Unlike GISA’s new ASP, the RSP submission format does not expand; the codes and validation within existing fields are updated.

First, the addition of Gender X enhances driver-level classification granularity, influencing premium calculations and, in turn, affecting how ceded premium is segmented and allocated within the pool. Next, legacy Ontario accident benefit codes, which were numeric, are deprecated in the relevant premium and claim coverage-code fields, which must be left blank in submission post-reform. Furthermore, optional benefit selections are captured using new grouped opt-in/opt-out codes within the existing optional coverage selection fields. Finally, the addition of a dedicated renewal indicator distinguishes renewals from new submissions, and a transaction code for cancellation of renewal further clarifies lifecycle reporting while heightening the need for precise transaction typing, because premium and exposure must be attributed to the appropriate policy event. These distinctions prevent renewal premium that never becomes effective from entering the pool and ensure that cancellation events, whether at renewal or mid-term, properly adjust ceded premium and exposure, preserving financial and reporting integrity within RSP.

Timing and Transfer Sensitivity

At its core, RSP allocation is governed by policy effective dates, written premiums, and exposure — variables that together dictate how risk is designated, timed, and reflected within the pool. Since coverage application under Ontario’s auto reform is tied to policy effective date, renewal timing plays a greater role in distinguishing pre- and post-reform business within RSP submissions. In the new reform, the policy effective date becomes even more important when optional benefit selections are expressed through grouped codes in current RSP fields and when legacy Ontario AB coverage codes are discontinued — as both changes increase reliance on correct transaction identification earlier in the workflow. While carriers may continue to operationally process renewals in advance, RSP eligibility and reporting remain anchored to effective dates and prescribed transfer windows, increasing the importance of accurate transaction identification.

In practice, this sensitivity is most visible in scenarios that require special handling. If a transfer date falls outside permitted timing parameters (for example, due to an attempted backdate beyond the allowable window), premium and exposure may be reflected incorrectly in the Pool, creating downstream reconciliation risk when claims emerge. Similarly, if a cancellation date is entered in a way that would cancel coverage on or before the loss date of a reported claim, the transaction requires special handling because Pool claim alignment depends on coverage being valid for the loss period. By validating transaction types and timing rules before submission, regul8 helps carriers catch and correct reporting exceptions early, before they affect Pool premium, exposure, and claim alignment. By incorporating timing validation controls directly into the reporting workflow, regul8 ensures that only eligible exposure enters the RSP and that cancellation events appropriately adjust ceded premium on a forward-looking basis.

Futureproof your Auto Reporting

As Ontario’s auto reform reshapes coverage structure, classification logic, and reporting requirements, insurers that embed precision at the data and transaction level will be better positioned to manage operational strain that extends well beyond consumer choice. That’s where an evergreen reporting platform makes the difference. Hubio’s regul8 standardizes carrier source data from disparate environments, including Guidewire Cloud, into a consistent structure, and keeps downstream reporting logic current as statistical plans evolve, from GISA’s ASP updates to FA’s RSP reporting. For regul8 clients, reform-driven updates are delivered as part of the SaaS subscription model: regulatory upgrades are released as part of the platform rather than treated as standalone development initiatives. The result is a reporting operation that can absorb filing updates through normal release cycles, sustaining compliance without repeatedly rebuilding workflows.