Alberta Auto Reform 2027: How the Shift to Care-First and Grid Repeal Reshape Regulatory Reporting

Alberta’s 2027 auto reform revises more than benefit design: it modifies how insurers classify accident benefits, bodily injury, uninsured automobile, Grid risks, and RSP business across GISA and FA reporting. For carriers, the challenge is translating Care-First and Grid repeal into submission-ready reporting before the reform takes effect.

Effective January 1, 2027, Alberta’s auto reform does more than expand Care-First accident benefits; it also retires Grid, shifting pricing away from a capped-rate framework and toward more direct risk-based pricing.

For drivers, Bill 47’s Care-First model is intended to make injury benefits available faster through their own insurers while reducing the litigation costs that can put pressure on premiums. The move away from Grid pricing is also intended to support a more stable, risk-based premium system, so premiums more closely reflect driver risk rather than spreading some high-risk costs across the broader insured population.

For Alberta auto insurers, these reforms become a reporting challenge: more benefit categories to and claim-level attributes to capture and different General Insurance Statistical Agency (GISA) and Facility Association (FA) reporting logic to satisfy. For carriers using the Alberta Grid Risk Sharing Pool (RSP), Grid retirement also adjusts how previously Grid-rated business is accepted, tracked, and reported through the Pool to FA.

Key Reporting Requirements Create New Complexity

Alberta’s 2027 auto reform begins as a product and pricing reform intended to improve access to care and manage insurance costs for consumers; the reporting complexity comes next, as insurers must translate how injury benefits, pricing treatment, and Pool reporting interact into the statistical, Pool, and transition data required for submissions and reform monitoring.

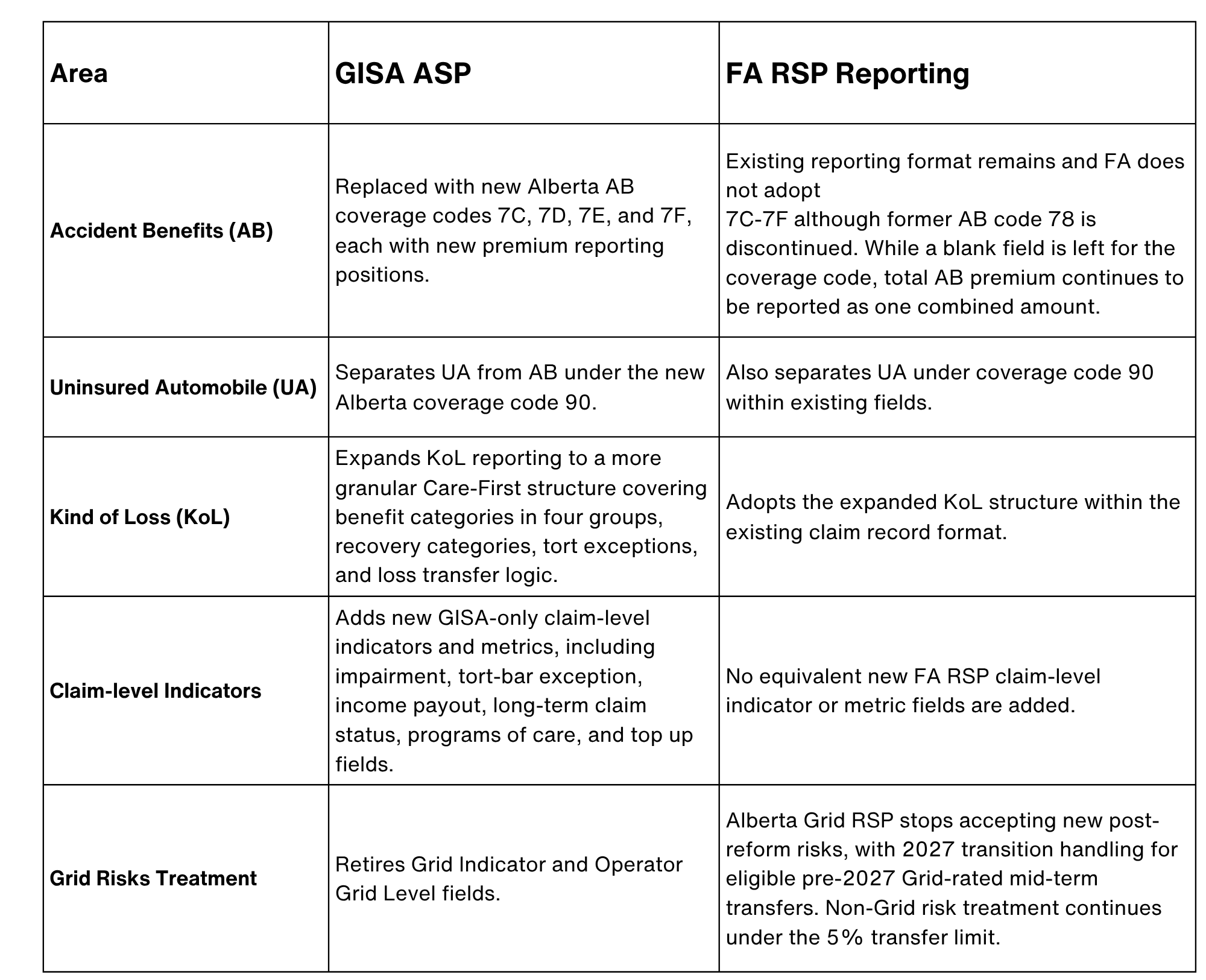

Where GISA uses the already-expanded 1,000-byte Automobile Statistical Plan (ASP) layout implemented for the Ontario auto reform for new Alberta fields, coverage codes, and claim-level indicators, FA takes the opposite approach: it keeps the existing RSP submission format unchanged but alters the code values, validation rules, and eligibility treatment within existing fields. That difference creates parallel reporting logic for insurers: the same source policy and coverage data must be translated into a more granular statistical reporting structure for GISA and a same-format, new-rules RSP structure for FA.

Two Reform Levers, Two Reporting Impacts

Whereas the Ontario auto reform was focused on optional benefits configuration and coverage reporting logic, Alberta auto reform creates reporting complexity across both the compensation model and the pricing framework. Care-First reshapes how injury benefits are classified, paid, and reported, while Grid repeal changes pricing treatment and RSP treatment for Grid-rated risks accepted through the Alberta Grid RSP. For insurers, the result is parallel reporting pressure: more granular statistical reporting for GISA and same-format, new-rule reporting for FA.

The reforms also affect core Alberta auto reporting areas, including Accident Benefits, Bodily Injury (BI) within Third-Party Liability (TPL), Uninsured Automobile (UA), and Grid and Pool treatment, while redefining how insurers classify benefits, capture claim-level attributes, apply coverage and Kind of Loss (KoL) codes, and satisfy parallel GISA and FA reporting rules.

How Care-First Reshapes Benefits Reporting

Under Care-First, the reporting shift follows the policy shift: accident benefits move into more defined first-party benefit streams, which means insurers must distinguish among benefit types more granularly at both the coverage and claim levels.

New and Retired Alberta Coverages

Pre-reform, the Accident Benefits category was reported under one coverage code. Going forward, that single numeric code is replaced with four new groupings: 7C, 7D, 7E, and 7F, respectively, health care and related expenses (HC&RE), permanent impairment benefits (PI), income replacement and other monetary benefits (IR&OM), and death benefits and related expenses (D&RE). Uninsured Automobile is also split out from Accident Benefits into its own coverage code with corresponding premium and claim reporting fields. Together, these revisions to the two coverages represent the Alberta auto reform’s biggest structural coverage transformation.

Expanded Kind of Loss Reporting

Beyond the coverage code revisions, Kind of Loss is rebuilt around Care-First. The expansion from five codes before the reform to 47 under Care-First reflects a more granular view of how injury benefits are delivered, tracked, and recovered. The 400s capture care, expense, impairment, death, and rehabilitation benefits while the 600s mirror many of them as loss transfer recoveries. The 800s represent income replacement and other monetary benefits, followed by the 900s as the corresponding loss transfer recovery benefit of each one. The expansion is a more detailed way for insurers to distinguish between benefits paid directly under the claim and amounts recovered through inter-insurer loss transfers.

New Claim Indicators

The Alberta auto reform adds new GISA-only claim indicators and values that build a more detailed claim profile. These fields are not mutually exclusive; where applicable, multiple indicators may describe various attributes of the same claim, including catastrophic impairment status, permanent impairment status, permanent impairment rating, tort-bar exception status, income payout, long-term claim status, and programs-of-care utilization. In practice, that detail

comes from combining claimant-count indicators, a percentage rating that captures impairment severity, numeric income values, and status fields that show whether specific exception, payout, settlement, or care-utilization conditions apply.

How a New Compensation Model and Grid Repeal Affect Pooled Business Reporting

Complementary to Care-First’s redesign of Alberta’s benefits and claims model is the elimination of Grid, which changes the pricing framework for previously Grid-capped drivers. For RSP reporting, the two levers affect different parts of the workflow: Care-First revises the coverage and Kind of Loss logic that must be reported within FA’s existing format, while ending Grid affects how certain ceded risks are treated through the Alberta RSP.

Same Format, New Rules

On the Care-First side, FA does not mirror GISA by adding the new Accident Benefits coverage codes to the unchanged RSP submission layout. Accident Benefits continue to be reported as one combined premium amount, even as the former single numeric AB coverage code is discontinued. Uninsured Automobile separates into its own coverage under the same new code used by GISA, while the expanded Kind of Loss structure is also adopted within the existing claim record format.

Grid-Related Field Retirements

On the GISA side, the Grid Indicator and Operator Grid Level fields are discontinued with no replacement, in line with Alberta’s move away from Grid-based rating. For RSP reporting, however, FA’s own Grid Indicator continues to be accepted during the 2027 transition for eligible mid-term transfers of pre-2027 Grid-rated risks.

Transition Rules and Life-of-Claim Consistency

During the transition period, FA’s guidance establishes two practical control points. First, for claims that fall under FA’s 2027 transition treatment, FA accepts either the pre- or post-reform Coverage and Kind of Loss structure, but that flexibility is not simply a cutover from old codes to new codes; once a claim starts down one reporting path, any subsequent claim activity must remain aligned to that path. Second, the Alberta Grid RSP continues to accept eligible mid-term transfers of pre-2027 Grid-rated risks during 2027, while new policies and renewals effective on or after January 1, 2027 fall outside the Grid RSP as Grid is phased out. The separate Alberta Non-Grid RSP remains governed by its own rules and is not part of the Grid RSP transition treatment.

Auto Reporting Peace of Mind with regul8

Alberta auto reform makes clear that regulatory reporting change is not limited to new codes or field positions. For insurers, this is where an evergreen regulatory reporting platform matters: it must be configurable enough to reflect how a carrier writes business upstream, while applying updated statistical plan, Pool, and transition rules downstream so submissions remain accurate, complete, and compliant as requirements evolve. The reform also broadens what insurers must capture and how they must classify, validate, and submit it across policy, coverage, claim, and Pool reporting workflows. For many insurers, source data may sit across multiple environments, including Guidewire Cloud and other core systems, where Care-First benefit categories, claim attributes, loss transfer activity, and ceded risk treatment may not map one-to-one into GISA ASP or FA RSP reporting.

Hubio has completed its analysis of Alberta’s auto reform requirements and is actively incorporating the required statistical reporting updates into regul8. regul8 is designed to manage that translation from upstream business logic to downstream regulatory output. As Alberta’s reform brings new coverage codes, expanded Kind of Loss logic, GISA-only claim indicators, retired Grid fields, and FA RSP transition rules, regul8 enables carriers to standardize source policy and claim data into reporting-ready structures aligned to GISA and FA requirements — reducing the need for manual rework as statistical plans and FA RSP rules evolve. With Ontario and Alberta reforms now reshaping auto reporting, insurers that build precision into their reporting operations today will be better positioned for the next wave of provincial change.